US Importers Owed Billions Following SCOTUS IEEPA Ruling: Is Your Recovery Plan Ready?

![]() By Barsha Bhattacharya

13 March, 2026

Blogging

Last Updated on: March 16th, 2026

By Barsha Bhattacharya

13 March, 2026

Blogging

Last Updated on: March 16th, 2026

Key Takeaways –

- Companies need to fast on refunds – Companies that have paid the IEEPA-based duties have potential refund claims, but statutory deadlines are ticking. However, business owners should map the exposure, quantify opportunities, and file protective claims now.

- Keep in mind other tariffs still apply – This decision only invalidated IEEPA-based tariffs. Tariffs under Sections 232, 301, and 122 of the 1974 Trade Act remain in force, and the administration is already signaling plans for new global tariffs.

Businesses need to update their financial models – Tariff refunds flow through cost of goods sold, which affects taxable income and effective tax rates. Business leaders should review their transfer pricing models and contracts to determine which parties receive refund proceeds.

The landscape of American trade underwent a seismic shift on February 20, 2026. In a landmark 6–3 decision, the U.S. Supreme Court ruled that the International Emergency Economic Powers Act (IEEPA) does not grant the Executive Branch the authority to impose independent tariffs.

Therefore, the verdict was a total rebuke of recent trade policy, effectively invalidating every IEEPA tariff ruling duty collected since February 2025.

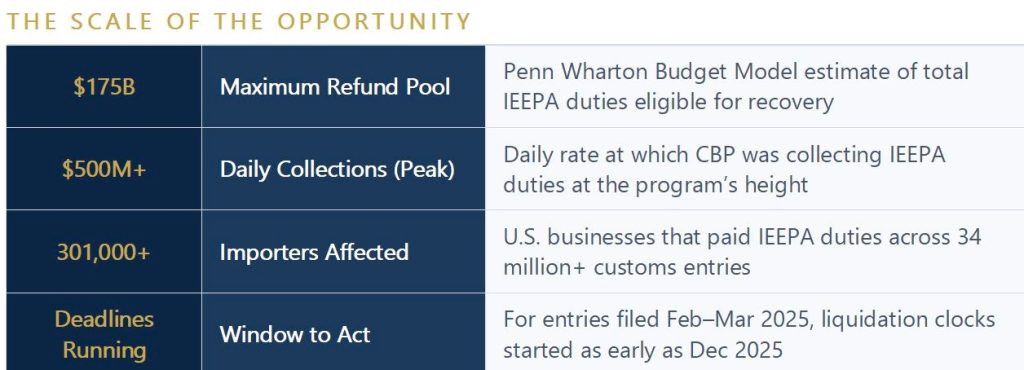

While the legal victory is won, the financial recovery has just begun. Customs and Border Protection (CBP) estimates the pool of recoverable duties at $130 billion, while Penn Wharton projections suggest the total exposure could climb as high as $175 billion.

Consequently, corporate tax and trade leaders must now move quickly to preserve refund claims while building resilient strategies for the next wave of tariff changes already in motion.

What Actually Happened?

In Learning Resources, Inc. v. Trump, the Supreme Court said last month that President Donald J. Trump went too far by using the IEEPA, a statute designed for genuine national emergencies, to impose broad, peacetime tariffs.

Therefore, the Court’s message was blunt: If you want sweeping tariff authority, get the U.S. Congress to give it to you explicitly. IEEPA doesn’t cut it.

Meanwhile, this ruling invalidated the tariffs that relied solely on IEEPA, including certain reciprocal global duties and some measures targeting Canada, Mexico, and China.

However, here’s the catch: Other tariff regimes, such as those outlined in Sections 232, 301, and 122 of the Trade Act of 1974, are still standing. Those weren’t touched by this decision, and they’re not going away.

The “Automatic Refund” Myth

Despite the high court’s ieepa tariff ruling, there is no “automatic” reimbursement mechanism. Meanwhile, for the 301,000 U.S. importers who paid these duties across 34 million entries, the path to liquidity is a procedural minefield.

“The government will not cut a single check automatically,” warns David King, Deputy CEO of Occams Advisory, an Inc. 5000 firm that recently launched a dedicated recovery platform.

“Every dollar recovered will require meticulous documentation and, in many cases, active litigation. The clock is running right now.”

A Strategic Roadmap To Recovery

To manage the complexity of this “refund recession,” trade experts are pointing toward integrated recovery models.

Meanwhile, Occam’s Advisory, for instance, has deployed a four-pillar program designed to move importers from assessment to cash-in-hand:

1. AI-Driven Quantification

The first hurdle is data. Importers must identify exposure by entry, HTS code, and liquidation status.

Therefore, utilizing AI-powered calculators to parse ACE portal data (specifically ES-003 Entry Summary CSVs) allows firms to distinguish between:

- Unliquidated entries: Eligible for Post Summary Corrections (PSCs).

- Liquidated entries: Subject to the strict 180-day CBP protest window.

- Aged entries: Requiring Court of International Trade (CIT) litigation.

2. The Shift To CIT Litigation

Recent guidance suggests the standard CBP protest pathway may be inadequate for IEEPA tariff ruling challenges.

Legal strategy is shifting toward the U.S. Court of International Trade (CIT). Importers are encouraged to assemble complete documentation packages, including CBP Form 7501s, commercial invoices, and certificates of origin, for submission to active dockets.

3. Claim Monetization & Financing

With CIT judgments potentially taking 12 to 36 months, “waiting it out” isn’t a viable option for every balance sheet. However, a new market for litigation financing has emerged.

Market Note: Institutional investors are currently purchasing IEEPA refund claims for approximately 40 to 45 cents on the dollar, providing immediate working capital in exchange for the eventual government payout.

4. Navigating The Tax Fallout

An IEEPA tariff ruling refund is not “found money”; it is taxable income. Refunds typically reverse previously deducted duty expenses into gross income in the year of receipt. However, this has significant implications for:

- Firstly, intercompany transfer pricing.

- Secondly, estimated tax payments.

- Thirdly, supplier contracts (specifically “tariff pass-through” provisions).

Why Speed Is Essential?

The administration has already signaled it will contest refund obligations, replacing the struck-down duties with a 15% Section 122 global surcharge. As the government prepares for years of litigation, importers face three critical risks:

- Expiring Protests: For entries filed in early 2025, the 180-day protest clock is already ticking.

- Plaintiff Status: Government stipulations for refunds often only apply to named plaintiffs in CIT filings.

- Pricing Risk: As the timeline grows more uncertain, litigation finance terms are expected to become less favorable.

Who Is At Risk?

The ruling affects any U.S. business that served as the Importer of Record for goods subject to IEEPA tariff ruling duties (including reciprocal tariffs on China, Mexico, and Canada, as well as specific surcharges on India and Brazil) between February 2025 and February 2026.

However, for mid-market manufacturers and retailers, the window to act is narrow. “We built our program to democratize the quality of counsel usually reserved for the Fortune 500,” says Anupam Satyasheel, Founder and CEO of Occams Advisory. “The legal foundation is solid. What businesses need now is execution.”

Are you eligible for a portion of the $175B recovery? Importers can begin their assessment using the Occams AI IEEPA Refund Calculator or schedule a consultation to review their CIT filing status.

The Bottom Line

The Supreme Court’s decision closed one chapter of the president’s tariff story, but it didn’t end it.

While for corporate tax and trade leaders, the message is straightforward: Grab the refund opportunity, protect your position, and use this moment to build a more resilient strategy for whatever comes next.

However, the most important thing you need to know is to reassess your IEEPA tariff ruling balances and disclosures. Therefore, if refunds are probable and you can estimate them, that may affect liabilities, expense recognition, and reserves.