Post Office Scheme For Women – A Complete Guide To Secure Monthly Income

![]() By Nabamita Sinha

22 September, 2025

Finance

By Nabamita Sinha

22 September, 2025

Finance

Today, women donning many hats in one go—professionals, caregivers, homemakers, and investors. Better financial security and independence have increasingly become indispensable for woman of any age group.

Among the many saving options available in India, Post Office Monthly Income Scheme (POMIS) is one of the most secure and reliable investment options.

It is especially appropriate for women looking for a fixed monthly return with minimum risk with the safety of their savings under a government-insured scheme.

In the following article, we shall analyze all you want to know about post office schemes for women, specifically the Post Office Monthly Income Scheme (POMIS), its advantages, suitability, process, regulations, taxation, and alternatives.

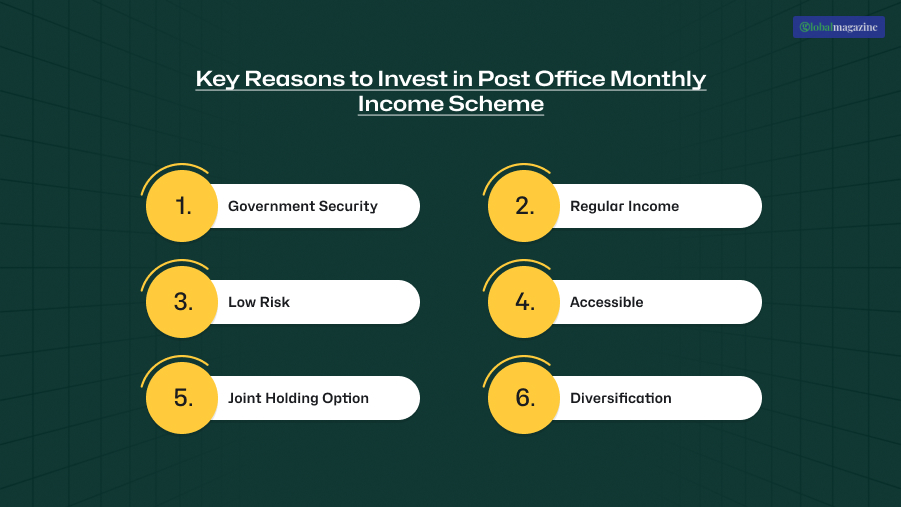

Key Reasons To Invest In The Post Office Monthly Income Scheme

The following are the reasons why ladies can rely on POMIS as a safe investment instrument:

- Government Security – Secured by India Post and the Ministry of Finance for the safety of deposits.

- Regular Income – Monthly payment of interest ensures a regular income.

- Low Risk – POMIS is different from equity or market-linked products in that it offers fixed returns.

- Accessible – Post offices are found in rural and urban India, and therefore, women all over are within easy reach.

- Joint Holding Option – It is possible to open joint accounts with a spouse or children for better financial planning.

- Diversification – Works as a conservative asset in an investment portfolio.

Highest Post Office Monthly Income Schemes For Women

Now, the Post Office Monthly Income Scheme (POMIS) is the top product for women seeking a monthly income. Its features are:

- Lowest Investment Amount: ₹1,000

- Highest Investment Amount: ₹9 lakh per individual account, ₹15 lakh per joint account

- Rate of Interest: Quarter reviewed by the government (as around 7.4% annually as of 2025, may be revised)

- Term: 5 years

- Payout: Monthly interest credited to the savings account directly

- Mode of Investment: Cheque, demand draft, or cash at the post office of choice

Eligibility And Process Of Opening An Account By Women

Any lady can invest in POMIS if she meets the eligibility criteria of India Post.

Who Can Open POMIS Account?

- Resident Indian ladies aged 18 years and above.

- Minors (when a guardian or parent opens account in her/his name, especially mothers).

- Joint Accounts – Women can open jointly with a maximum of three adults.

- Senior Women Investors – Women above 60 years can invest, but they can also look into SCSS (Senior Citizens Savings Scheme).

Related Resource: Which Sector Is Growing Fast In India For Investing In 2025?

Woman Applicant Documents

To open a POMIS account, the following documents are needed:

- Identity Proof – Aadhaar Card, PAN Card, Passport, Voter ID, or Driving License.

- Address Proof – Aadhaar, bill, passport, or ration card.

- Passport Size Photos (2–3).

- PAN Card – Mandatory for deposits over a limit.

- Birth Certificate (children) if the account is opened under their name.

Step-By-Step Account Opening Procedure

Here are the steps you need to follow if you wanna open an account. Just follow each step to make the process easier.

- Visit the Post Office – Go to the closest post office with documents.

- Get the POMIS Application Form – Available at the branch or download from the website.

- Give Details – Name, address, nominee, amount of deposit, and other details.

- Support Documents – Give copies of identity and address proof along with passport-sized photos.

- Deposit Amount – Pay in the initial deposit (minimum ₹1,000).

- Account Opening – The Account gets opened after processing and interest from next month.

Rules, Taxation, And Withdrawal Facilities

When it comes to the rules, taxation, and withdrawal facilities, here are the things that you need to keep in mind.

- Tenure – Locked for 5 years.

- Premature Withdrawal – Allowed after 1 year with penalties (see below).

- Taxation – Interest received is taxed as “Income from Other Sources.”

- TDS – No TDS at source, but investors must return the income in ITR.

- Nomination Facility – Can be made at the time of opening or later.

- Account Transfer – Transferable among different post offices in India.

Tenure, Premature Withdrawal, And Penalty Details

- Tenure – Locked-in 5-year term.

- Premature Withdrawal –

- Allowed after 1 year but before 3 years: 2% penalty on deposit.

- Allowed after 3 years: 1% penalty on deposit.

- Maturity Options – On maturity, investors can withdraw the entire deposit or redeposit into other small savings schemes like SCSS or NSC.

Taxation On Interest Earned

- Interest Income Taxable – Part of the individual’s income for the year.

- No Section 80C Benefit – Unlike PPF or NSC, POMIS deposits aren’t deductible under Section 80C.

- Best For Women in Lower Tax Brackets – Since the scheme is risk-free, it is apt for women in a 5%–10% tax bracket.

Account Transfer And Nomination Facilities

- Account Transfer – Women can easily transfer their POMIS account from post office to post office, allowing them to move around in case they change residence.

- Nomination – Nominee can be notified at the time of opening the account. In case of the death of the account holder, the nominee will get the proceeds.

Best Alternatives To POMIS For Regular Income

While POMIS is a safe option, women can also opt for the following:

1. Bank Fixed Deposits With Monthly Interest Option

- FDs are provided by banks with monthly payment of interest.

- Greater flexibility, but based on bank-specific interest rates.

2. Government Floating Rate Savings Bonds

- Guaranteed by the Government of India.

- Interest is reset every 6 months tied to NSC rates.

- Minimum lock-in of 7 years.

3. Senior Citizens Savings Scheme (for Women above 60)

- For senior women investors.

- Higher interest rates (around 8.2%).

- 5-year lock-in with a premature withdrawal facility.

4. Monthly Income Plans from Mutual Funds

- Market-linked, which can give potentially better returns.

- For women with moderate to high risk-taking capacity.

- Less secure than POMIS but safe for diversification.

Knowing Each Scheme

Post Office Monthly Income Scheme (POMIS) is one of the most secure and reliable savings instruments for women to achieve a stable income with low risk.

Whether you are a homemaker who desires assured returns, a professional woman who plans a secondary source of income, or an elderly person who wishes to invest securely, POMIS is an excellent option.

With guaranteed government backing, easy account opening, pan-India presence, and guaranteed returns, it makes women investors invest confidently towards securing their financial future.

However, women should also look at alternatives like bank FDs, government bonds, SCSS, and monthly income schemes of mutual funds to form a diversified portfolio. The plan is to align investments with one’s financial goal, risk profile, and monthly income needs.